Whenever a new technology emerges in the market, mixed opinions arise from the techies. Few flags that as a disaster while few claim that as a lifesaver. Blockchain is not an exception to it. There come Solution Providers who utilize the opportunity by busting a few unresolved queries; declare themselves as the best in the industry and play the money-making game.

While the rest of unaddressed queries remains as MYTHS. Myths remain as myths because of 2 major reasons. Either we don’t have time to analyze and just ride the wave or we are afraid of losing something as a cost of doing so.

Let’s break a few blockchain myths today!

Myth 1: Blockchain is costly

Partially True

Blockchain implementation depends on lots of factors like

- The complexity of the problem

- The number of stakeholders involved in the network

- Need for integration with existing systems/products

- Migration of an existing system to the blockchain platform

- Need for 3rd party service providers (AWS, Twilio, etc.)

- Maintenance, etc.

Based on the requirements, the cost may vary.

Myth 2: Blockchain is only for Financial Services

Not At All

This myth remained unbroken for a very long time. Now it has crossed its horizon and stepped into every possible field of service.

Healthcare service providers are keen in using blockchain especially in telemedicine services.

Recently Supreme Court of India curbed its restrictions on cryptocurrency trade-in India. Tamilnadu Govt. joined the initiative and is aiming to develop a state-wide blockchain to enable all the Govt. entities to avail the transparency and security. Extending its use to other departments may soon be legal based on its implementation success.

Myth 3: Blockchain is nothing but a cloud-based database

False

Blockchain is a set of nodes(internet-enabled computers) which registers the timestamps of transactions. It is a tamper-proof digital ledger. The stakeholders are updated on the new transactions with Proof of Existence but not the actual documents like the cloud-based database.

Myth 4: Private Blockchains are secure than Public Blockchain

False

Public blockchains are decentralized, meaning any participant who is willing to participate can participate using the protocol when all the stakeholders approve it. All the stakeholders are owners of the entire network. More number of participants makes the information available at multiple nodes. The more the number of participants more is security.

Whereas the private blockchains, on the other hand, are invitation-only networks where the ownership rests with one. This makes the network centralized. Private blockchains are faster as the authentication takes lesser time. But it is less secure as the number of nodes is less.

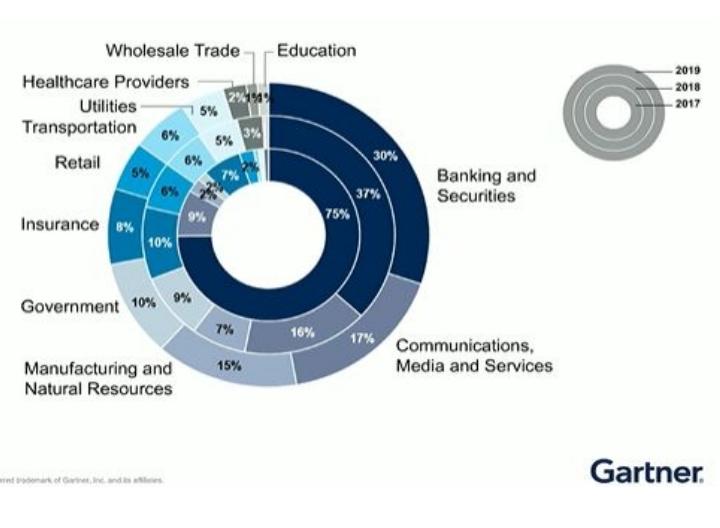

Best Part of Blockchain is Yet to Come

As per Gartner’s prediction, Investments on Blockchain will be more from 2022 and large scale economic value will be seen from 2027 across the globe. To the surprise, the number of live blockchain cases is more in the APAC region than any other country in the world and by 2023, blockchain will support $2 trillion goods and services management & tracking per annum.

Let’s see more interesting facts and myths about blockchain in future articles. Stay tuned with KriyaTec Blogs.